How BPI Evaluates Software & AI Startups

The new normal

In 2011, a16z declared “software is eating the world”. By 2025, first voices claimed that AI is eating software. In early 2026, fear became reality as the launch of Claude Cowork triggered the “SaaSpocalypse”, wiping ~$1T in software market cap within a single week (Reuters). Beyond incumbents, the selloff exposed a structural tension for anyone building AI-native products. Every model release poses the risk of turning what was a standalone product into a feature of a general-purpose LLM. This by no means suggests that general-purpose models can match the quality and depth of dedicated vertical players. But if they can achieve 80% of the output quality at a fraction of the price, that puts enormous pressure on margins.

So is software dead? Is vertical AI dead? And should investors simply put more money into leading AI labs? No. But companies’ right to win in the software market is fundamentally changing. We at Burda Principal Investments believe that traditional moat frameworks, like Helmer’s 7 Powers, still hold. Yet they fall short. They don’t account for the competitive threat of general-purpose LLMs, shifting build-vs-buy dynamics, or new pricing models. That’s why we extend them.

The additional four dimensions we screen before writing a check

After evaluating a wide range of software and AI deals over the past 12 months, we identified four dimensions that answer one key question: does this company have the structure for a moat to emerge, or is it a wrapper at risk of commoditisation?

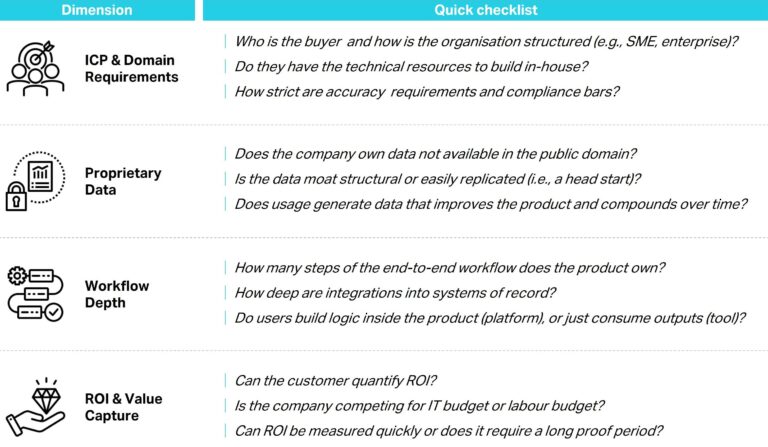

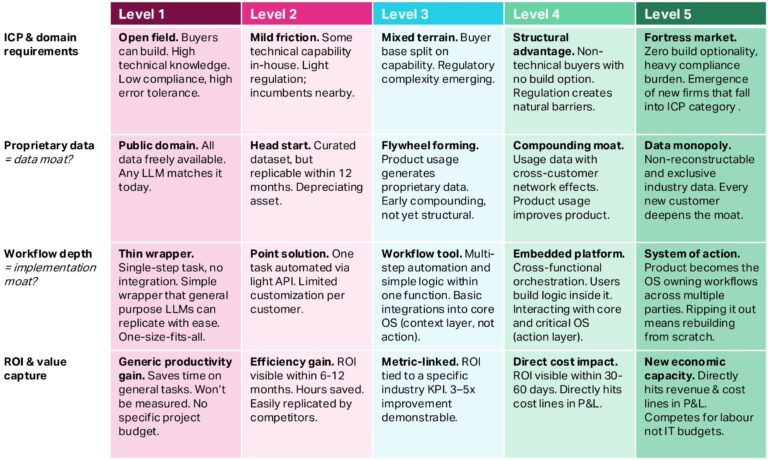

Dimension 1 – ICP & Domain Requirements: Who is the buyer and can they build the product themselves? The most defensible companies sell into markets outside of tech where buyers have no realistic build option, such as small law firms without engineering teams or healthcare providers navigating heavy compliance requirements. When your ICP is non-technical, operates in a highly regulated environment, and belongs to a fragmented, growing buyer base, you’re in fortress territory. Conversely, selling to companies with deep engineering resources and higher error tolerance puts you in a structurally weaker position from day one.

Dimension 2 – Proprietary Data: Does the company own data that isn’t available in the public domain and is the advantage structural or merely a head start? This is often the dimension with the most noise. Founders frequently claim a data moat; few actually have one. The critical distinction: data curated before launch (e.g., scraped, acquired) is a depreciating asset as it can replicate with ease. On the other hand, data generated through product usage that compounds over time and creates cross-customer network effects is a real moat. The question is not only “do you have proprietary data?”, but also “does every new customer improve your product?”

Dimension 3 – Workflow Depth: How many steps of the end-to-end workflow does the product own and how deeply is it wired into the customer’s systems of record? A single-step automation with no integration is a wrapper. A product that orchestrates multi-step workflows across legacy systems, where users build custom logic inside the system and switching means rebuilding from scratch, becomes a defensible platform. The deeper the integration, the higher the switching costs, and the wider the moat.

Dimension 4 – ROI & Value Capture: Can the customer quantify returns, and what budget is the product competing for? Efficiency gains are easy to replicate and hard to defend. Enablement ROI, where the product unlocks new revenue or creates economic capacity that didn’t exist before, is structurally stickier. The strongest signal is measurable P&L impact across both cost and revenue line items within the first month. If that is the case, companies can start competing for larger labour budget, not IT budget. However, this is a fundamentally different sale that founders need to crack.

Applying this framework, each company can be scored on a five-level scale from Level 1 (no moat) to Level 5 (structural moat potential), with the weight of each dimension being context-dependent. Investment decisions for Level 1 (pass) and 5 (continue) are straightforward. Deals at Level 3, where the structure for a moat is forming but not yet locked in, require strong investor judgement.

What this means for investors and founders

The question is no longer whether a software company uses AI, every company does. The question is whether the structure of the business creates defensibility that compounds as technology improves or erodes. Our framework won’t give you a definitive answer, but it will tell you where to look, what to pressure-test, and where the risk is hiding. In a market where the distance between a future category leader and a wrapper has never been thinner, that clarity matters.